Author

Written by: iPay

Sign Up

Send Verification Documents Contact Us Book a Demo Our Blogs

Posted on August 16, 2024

Why Having the Right Documentation Will Benefit Your Business in the Long Run

By: iPay

We understand—getting documentation can feel like yet another task to add to your businesses’ to-do list. But the truth is, it offers an array of advantages that make it well worth the time and effort. From making smart decisions, reducing risks, saving money to building trust with your clients and partners. In Kenya, compliance with statutory requirements is crucial, yet many businesses struggle with maintaining up-to-date records and meeting regulatory standards. You may have wanted to partner with a financial institution and get asked to send your application documents. Telling you that you need to meet certain requirements before opening an account or rather utilising their solutions. Some businesses hesitate to provide the necessary documentation, perhaps feeling that it's an unnecessary hurdle- but hey, the fact remains that you will not open that bank account without giving that documentation.

Just as our Senior Sales Representative Benson Nyongesa says, “Simply throwing around terms like KYC and AML isn’t helpful for businesses. This can sound like jargon to many business owners.” Instead, Benson focuses on breaking down what is required by these businesses to meet the regulatory requirements.

In payments, when we talk about KYC (Know Your Customer) and AML (Anti-Money Laundering), we're really talking about making sure that everything is in order and that you're following the rules. Let’s break down what KYC and AML is and why this it is so important:

1. KYC (Know Your Customer)

KYC, which stands for 'Know Your Customer,' is a process used financial institutions to verify your identity in compliance with KYC & AML regulations. In simple terms, it's like checking someone's ID to make sure they are who they say they are and not someone using a fake identity.

2. AML (Anti-Money Laundering)

Think of AML as a set of rules and procedures that businesses follow to prevent criminals from hiding illegal money and making it look like it came from legitimate sources. Imagine you run a shop. AML is like having security cameras and guards to make sure no one brings in stolen items to your shop and tries to sell them as new.

The objective of AML is to promote transparency in financial transactions and maintain the integrity of the financial system by preventing criminals from using it to launder their dirty money.

How the KYC Process Works

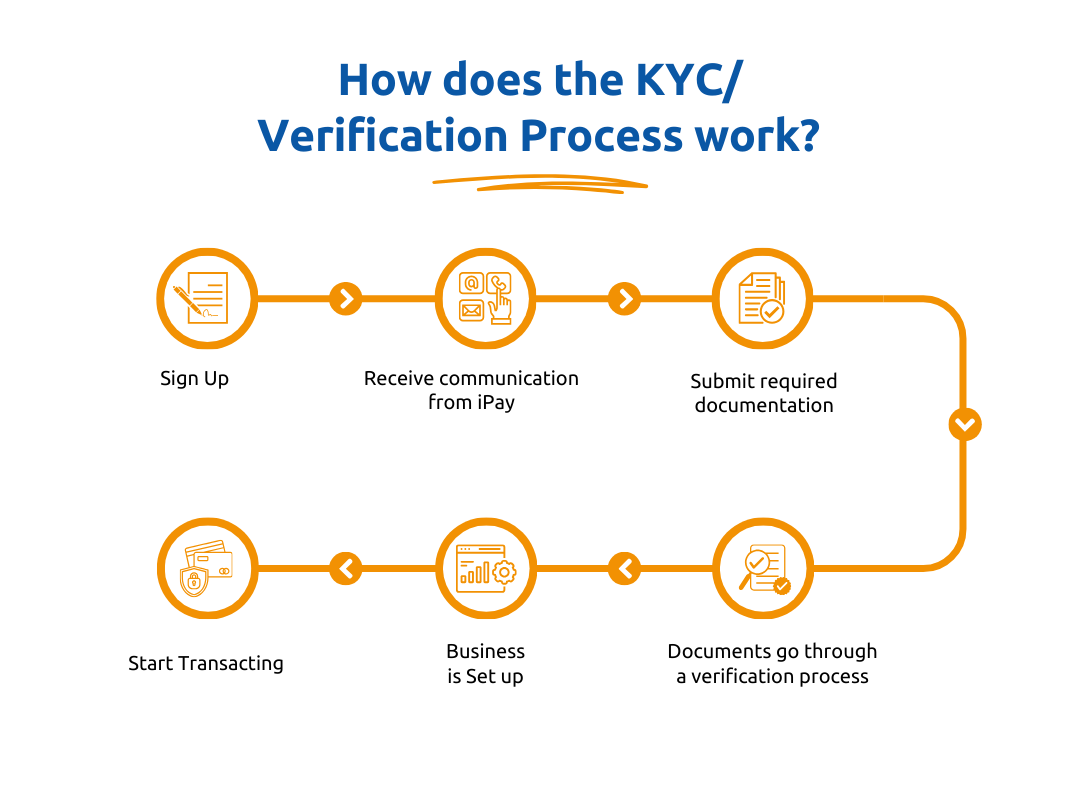

- Initial Verification: When you sign up with iPay, we ask for basic information about your business, including registration documents, identification for key personnel and financial details. This initial step helps us verify that your business is legitimate and meets our standards.

- Ongoing Monitoring: Over time, we may need to update our records, especially if your business undergoes significant changes or if certain documents expire. This ensures that our records are accurate and that we continue to comply with regulatory requirements.

Document Renewal: It's important to note that some documents, such as business permits, may expire and require renewal. For example, a single business permit in Nairobi must be renewed annually or licenses from regulators such as Tourism Regulatory Authority (TRA) that is also Keeping your documents up to date ensures compliance and smooth business operations.

Image: How iPay’s KYC process works

Image: How iPay’s KYC process works

Quote from our Group Compliance Officer:

"Getting the right records is not just about compliance—it's about building a trustworthy relationship with our partners. By ensuring that all documentation is correct, we can offer better services and maintain the high standards that our regulators expect."

I’d like to complete/update my KYC Verification Process

The Bigger Picture: Why KYC and AML Matter

Currently, Kenya is facing significant challenges with money laundering. The country has been placed on the Financial Action Task Force (FATF) grey list due to deficiencies in its anti-money laundering (AML) and counter-terrorism financing (CTF) frameworks. This means Kenya is under increased scrutiny and must make critical changes to its financial infrastructure to address these issues.

In response, Kenya has enacted new laws and tightened regulations, especially focusing on the financial sector. The AML act was amended in 2023 as a result, this amendment introduces new legal requirements and obligations that must be adhered to in order to remain compliant with the updated regulatory framework.

Globally, it is reported that countries with strict KYC and AML measures have seen a significant reduction in fraudulent activities, which has boosted customer confidence and business growth.

Conclusion

Proper documentation is the cornerstone of effective KYC and AML compliance. By addressing gaps and ensuring you have the right documents, you build trust with partners, enhance your credibility and protect your business from potential risks.

Sign up with iPay

Share your thoughts

Comments

Add new comment